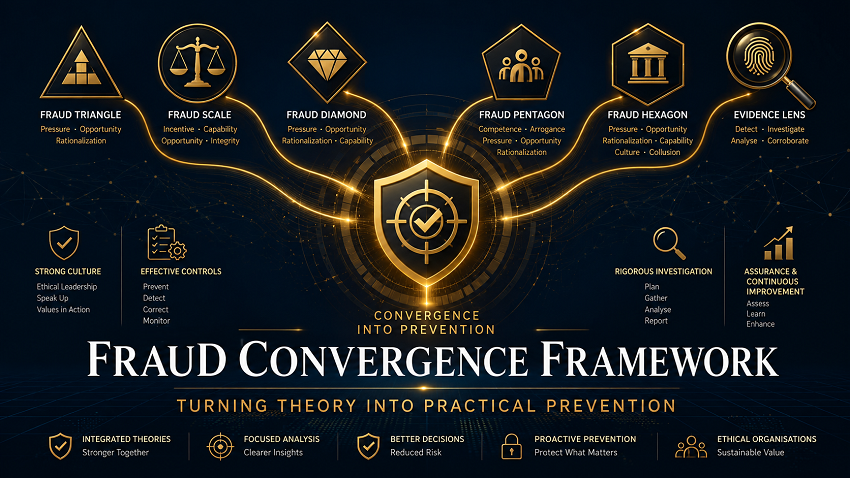

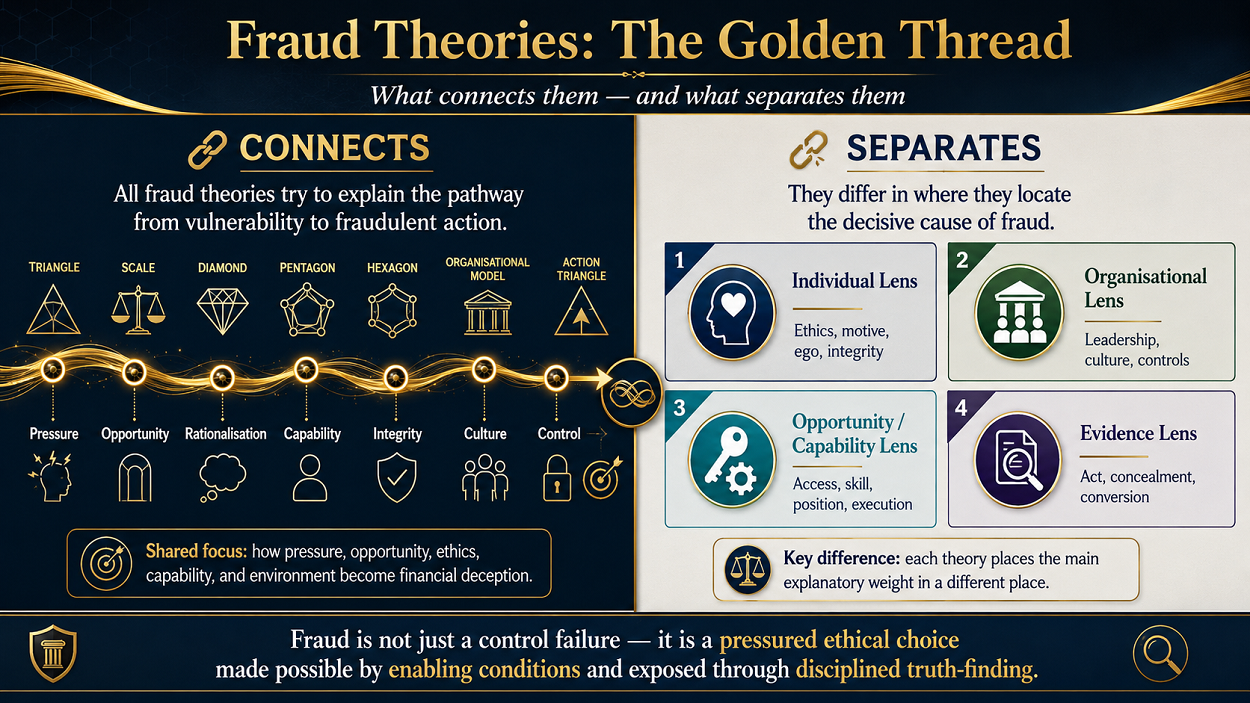

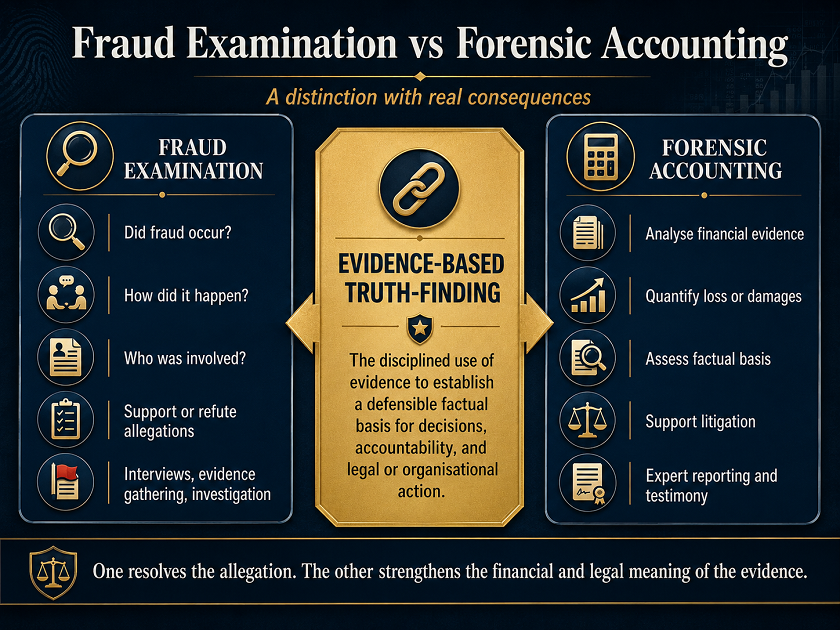

Analysis of Digital Accounting Education Literature From 1982 to 2023.

Editorial: Forensic Education

"An Analysis of Accounting Education Literature in the Digital Era."

This paper analyses the predominant trends in digital accounting education research. This bibliometric study of 287 indexed publications from 1982 to 2023 delineates significant topics, research trajectories, authors, keywords, journals, organisations, and countries that have shaped the discipline. It further suggests avenues for investigation.

The article asserts that accounting education must no longer see AI and other coming technologies as optional. Technologies that employ hybrid intelligence to enhance human judgement and decision-making should be included into the core curriculum. Higher education institutions could utilise seminars, internships, competitions, industry engagement, together with blockchain, cybersecurity, and big data analytics. These strategies facilitate the instruction of students on modern accounting principles and competencies.

The study also highlights colleges collaborating with professional accounting bodies to train professors in new technology. Accounting curricula must be revised to incorporate technology improvements as a component of quality assurance and accreditation protocols. Policymakers ought to advocate for curriculum reform, infrastructure enhancement, research institutions, and international collaboration. In underprivileged nations, enhanced assistance is necessary for data literacy, program transformation through practitioner involvement, and access to digital technologies like Tableau, Python, and SQL. The research revealed that scholars necessitate a conducive institutional culture and enhanced working environment to foster innovation and integrate new technologies into accounting education.

Source: Amin, H. M. G., Hassan, R. S., Ghoneim, H., & Abdallah, A. S. (2024). A bibliometric analysis of accounting education literature in the digital era: current status, implications and agenda for future research. Journal of Financial Reporting and Accounting, 23(2), 742–768. https://doi.org/10.1108/JFRA-12-2023-0802

Image: By Quillbot AI Image Generator