Fraud Examination vs Forensic Accounting: A Distinction with Real Consequences

Editorial: (Fraud Examination)

"Forensic Accounting vs Fraud Examination: Roles, Importance and Differences."

Fraud examination and forensic accounting are often used as interchangeable labels, but the distinction carries real consequences for organisations, investigators, legal teams and educators.

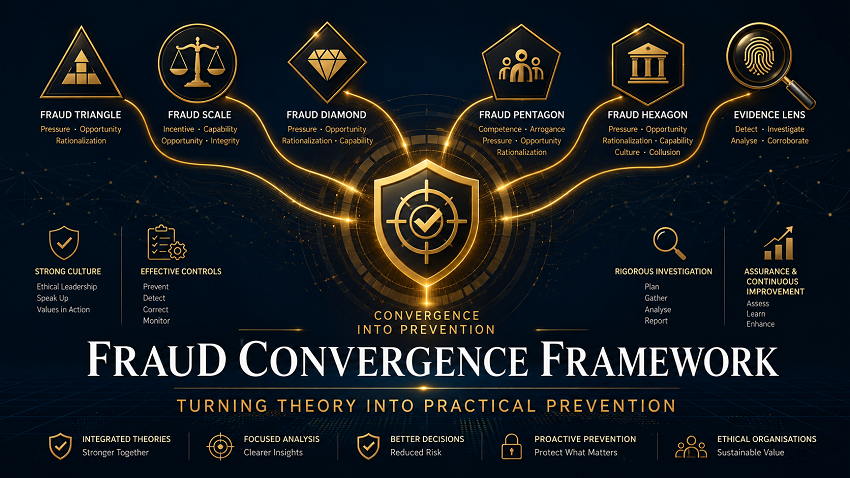

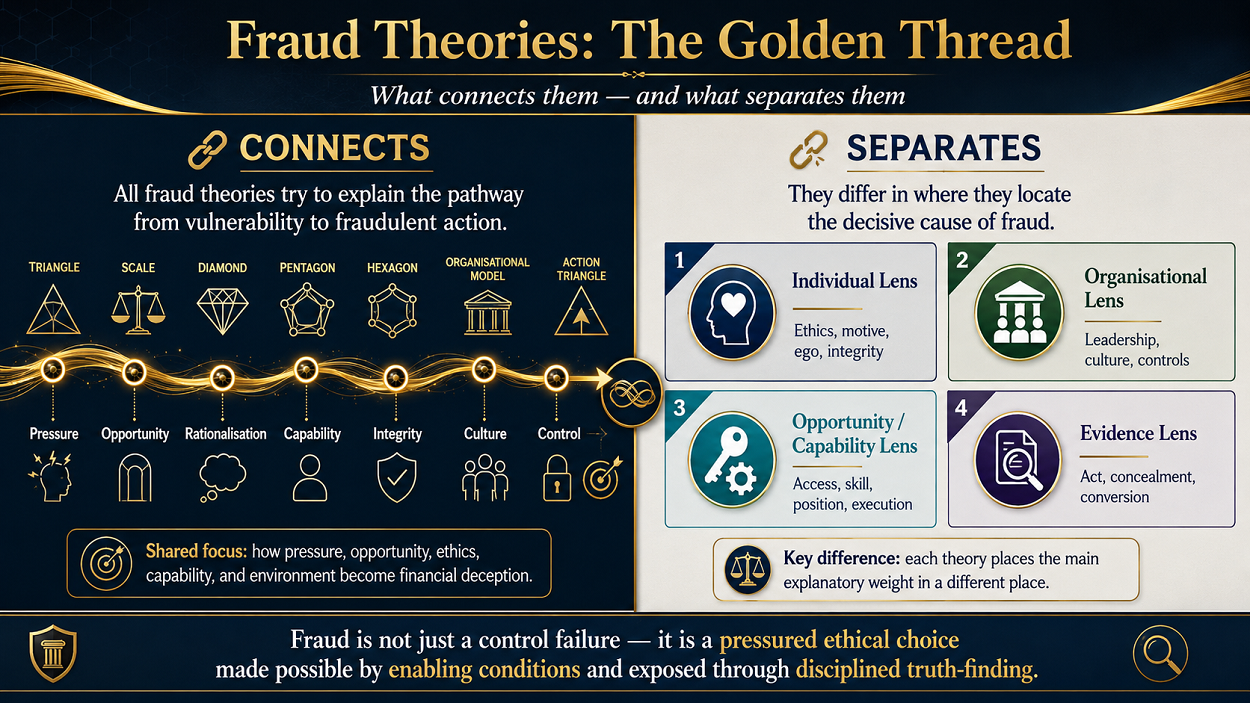

Tekavčič and Damijan (2021) usefully clarifies that fraud examination is primarily concerned with resolving allegations of fraud: whether fraud occurred, how it happened, who was involved, and whether the available evidence supports or refutes the allegation. Forensic accounting is broader. It examines financial evidence, tests the factual basis of allegations, quantifies financial consequences, supports litigation and may require expert testimony.

Yet the golden thread connecting both disciplines is evidence-based truth-finding: the disciplined use of evidence to establish a defensible factual basis for decisions, accountability and legal or organisational action.

This distinction is not academic hair-splitting; it affects the mandate, methodology, evidence strategy, professional skills required, report structure and legal defensibility of the findings. In practice, one of the most dangerous instructions remains the vague request to “conduct a forensic audit”. It sounds decisive, but without a properly defined investigative mandate, it can misdirect the process before the first document is even reviewed.

The real lesson is that modern forensic practice requires more than technical competence or professional labels. It requires clear scope, ethical independence, legally sound evidence handling, financial analytical ability, digital-era competence and the judgement to distinguish fact, inference and opinion. When this distinction is ignored, investigations risk producing findings that are impressive on paper but fragile under scrutiny.

Source:

Tekavčič, M., & Damijan, S. (2021). Forensic Accounting vs Fraud examination: Roles, Importance and Differences. Journal of Forensic Accounting Profession, 1(2), 29-47. https://reference-global.com/article/10.2478/jfap-2021-0007

Image: OpenAI. (2026). Fraud Examination vs Forensic Accounting [AI-generated User-Prompted image]. ChatGPT.